New Tax Legislation And New Opportunities For Planning

By: Randall A. Denha, J.D., LL.M.

The recently-enacted Tax Cuts and Jobs Act significantly changes the tax landscape, beginning on January 1, 2018. Many of these changes will sunset on January 1, 2026, when the law reverts to the pre-2018 law. Of course there is always a possibility things change again after the next presidential election in 2020 and Congress could, of course, enact new legislation that is less favorable in the meantime.

The new law affects every client’s estate plan in some way, and we strongly recommend that you review your current estate plan to confirm that your wishes will be carried out under the new law. The law also provides for significant new planning opportunities.

Estate, Gift, and Generation-Skipping Transfer Taxes

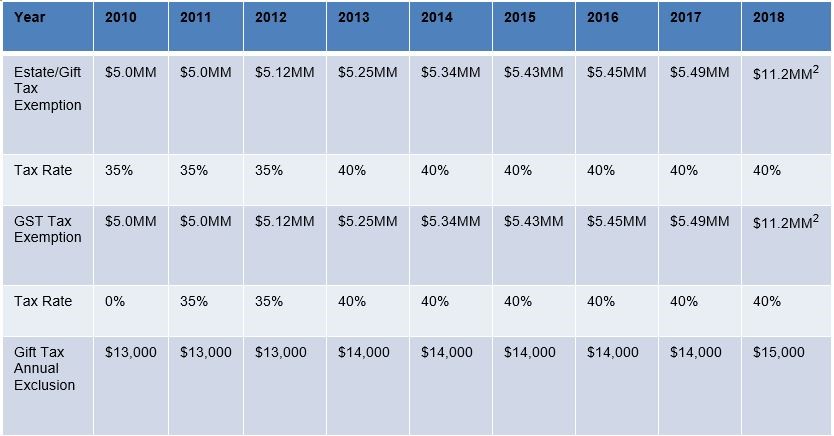

An individual’s estate and gift tax exemption has just doubled to $11.2 million per person beginning in 2018. This amount is adjusted for inflation and will increase each year until January 1, 2026, when the estate and gift tax exemption will revert back to $5 million, adjusted for inflation. The doubling also applies to the generation skipping transfer (“GST”) tax exemption. The doubling of the exemption sunsets after 2025 and the exemption reverts to $5 million indexed for inflation from a base year of 2016.This doubled exemption allows clients rare planning opportunities, discussed below. The chart below shows the changes in the estate, gift and GST tax exemptions, tax rates and annual exclusion from 2010 to present day:

As the concept of “portability” of estate tax exemption is retained, a married couple can now pass $22.4 million free of estate and gift tax (until the law sunsets). The top federal tax rate for both gift taxes and estate taxes remains at 40%. Planning now while the gift tax exemption is doubled may be viewed as a limited opportunity to upgrade or improve existing estate plans. With no assurance that a future administration will not negate the doubling of the estate and gift exemption, and where a future administration may prefer to substantially lower the exemption amounts, planning should not be deferred to a later date. Additionally, the new law retains the “step up” (or “step down”) in basis to date-of-death values for income tax purposes.

As we assumed, the gift tax annual exclusion has increased to $15,000 for each donor per donee.

All in all, it is estimated that only 1,800 of the 2018 decedents will have to pay estate tax in 2018 (with an estate tax exemption of $11.2 million) which is down from 5,000 decedents in 2017 (with an estate tax exemption of $5.49 million.)

Planning Recommendations and Opportunities

So with all of the above changes that have taken place in the law (and there are many), what tools and techniques can be used and what things should you be looking at when reviewing your planning? The following ideas, based on the following wealth levels, are overly simplified and generalized for purposes of this piece, but are meant to spur thought and discussion among you and your advisors:

Married Couples with assets under $5.5 million

• Leaving assets to the spouse outright at death or in a trust without restriction. By structuring the estate this way, the assets will receive a basis step up after the death of the surviving spouse thereby removing all capital gains tax and leaving the assets to the beneficiaries without additional income tax upon sale.

Married Couples with assets over $5.5 million but less than $11 million

• Upon the death of the first spouse, leaving the assets to the surviving spouse in a trust which allows an election to be made to disclaim the assets to a standby Family Trust to safeguard any estate tax exemption, if desired. The assets passing to the surviving spouse would pass into a Marital Trust which would be structured as a QTIP trust thereby protecting the assets in this trust from being taken by a future spouse to the detriment of the beneficiaries of the first spouse to pass away.

Married Couples with assets over $11 million but less than $22 million

• Similar planning to those with assets between $5.5 million and $11 million, but this class of persons may consider making gifts in a manner that allows for the other spouse to have access to the amounts so gifted. Techniques such as Spousal Lifetime Access trusts or Domestic Asset Protection Trusts should be considered.

• For all trusts and planning strategies used for estates with values that are less than $22 million, there needs to be an emphasis on flexibility being built into the documents. Keep in mind that the transfer tax exemption is set for a reset back to $5 million (indexed) after the year 2025.

Married Couples with assets over $22.4 million

• For these clients with net worth above $22.4 million, a 40% tax bite can still destroy a closely held business or a family legacy. For clients who continue to have estate tax exposure, re-calculating existing federal estate tax exposure under the new rules should be the first order of business. Thereafter, to the extent needed, the traditional wealth transfer strategies should continue to work. Continuing making gifts using the increased exemption will enable clients to remove further assets from their taxable estates and exempt any future appreciation from transfer taxation.

• Clients should review whether transfers should be made from any trusts to which GST exemption had not been allocated to take advantage of the additional GST exemption amount available (whether distributions from GST non-exempt trust to GST exempt trusts would be a good idea). It may also be prudent to make a late allocation of GST exemption election to existing non-exempt trusts so that if a future administration rolls back the Act’s benefits, those trusts will be GST exempt trusts.

• The following opportunity shifting, transfer and freeze planning techniques can be considered:

o Annual exclusion gifts to the children and grandchildren

o Forgiveness of outstanding loans to children

o Gifts to dynastic trusts for the benefit of children and grandchildren or making a late allocation of GST exemption to an existing trust

o Sales to defective trusts which under current law can be significantly magnified to permit a gift of $22.4 million of assets and a sale of over $200 million in assets subject to a promissory note

o Grantor Retained Annuity Trusts, or GRATs

o Qualified Personal Residence Trusts, or QPRTs

o Transfers from QTIP marital trusts

o Life insurance transfers to or from an insurance trust

o Technique to Consider-Upstream Gifts can be made to a parent(s) of a client who may not have any concern over estate tax. One normally doesn’t think of making gifts to a parent, but this type of gift permits one to gift assets to a parent and then having those same assets left to you (estate tax free). You can receive the assets back with a new income tax basis and all appreciation removed, subject to other tax laws which may restrict such technique depending on the facts. The Upstream technique can be used for clients in any size estate for this income tax play.

Clients should review their estate planning documents to confirm any formula language in their existing documents will be interpreted as intended in light of the new law. For example, language in existing documents creating a marital trust for a spouse and a family trust for the children may now result in the marital trust receiving nothing simply because the estate exemption amount has doubled! Alternatively, leaving the amount that can pass free of GST tax to your grandchildren with the remainder of your estate going to your favorite charity may now result in the charity receiving nothing simply because the GST exemption amount doubled! Due to changes under the Act, will and revocable trust dispositive provisions may not function as planned.

Regardless of the asset size of one’s estate, some couples still hesitate to make transfers of assets to their children preferring instead to continue benefits for the grantor (and his/her spouse, if married), but would still like to take advantage of the generous exemption under current law before a change in the law. The following are a few specific strategies that can be utilized by this group of clients:

• Spousal Lifetime Access Trusts, or SLATs (previously written about and can be accessed at https://denhalaw.com/spousal-lifetime-access-trusts-good-for-you/

• Inter-vivos QTIP Trusts

• Domestic Asset Protection Trusts

• Establishing a Management Company and paying fees to a grantor

All in all, depending on how your planning is structured, the increased exemption levels could drastically alter the disposition of your estate. Because of the significant changes in the estate tax laws, we encourage all clients to review and revisit their estate plans.

• For some clients, the substantially larger exemptions mean that their estates will no longer be subject to estate tax in the future. Those clients might consider unwinding more complicated, tax-focused trust structures and simplifying their estate plans.

• For clients with larger estates, the increased exemption means that they have additional opportunities to make gifts to children, grandchildren, and other beneficiaries without incurring gift tax.

• Clients with interests in closely-held businesses can consider additional planning involving the use of grantor retained annuity trusts (GRATs) or sales to grantor trusts.

• Clients may want to consider making late allocations of GST exemption to trusts that are not exempt from GST tax.

• Clients should review formula clauses where the amount passing to a class or group of beneficiaries is tied to the estate tax exclusion amount, as the significant increase may result in more passing to that group of beneficiaries than was originally intended.